AI Supercycle Ignites 2026: Fed Rate Cuts Fuel the Fire as ASML Explodes, Memory Prices Soar, and Private Valuations Go Nuclear

By Cash Flow University · · 6 min read

Explore how AI supercycle in 2026 is fueled by Fed rate cuts, ASML's growth, and soaring memory prices.

January 8, 2026 – The AI boom isn't cooling down. It's accelerating into overdrive. Lower interest rates, exploding demand for advanced chips, and private valuations hitting absurd heights are all converging right now. From Anthropic's meteoric rise to ASML's monopoly grip on the future of semiconductors, from memory prices breaking historical cycles to the Fed's dovish pivot, we're witnessing a once-in-a-generation convergence of forces that could redefine tech investing for years to come.

I want to break down the four major catalysts driving the AI supercycle in 2026: the insane private market valuations, the infrastructure enablers dominating public markets, the memory semiconductor surge, and the macroeconomic tailwinds that could fuel this rally for the entire year.

1. Private AI Valuations Are Getting Ridiculous

The money pouring into frontier AI companies shows zero signs of slowing. We're talking about valuations doubling in a matter of weeks. Not months. Weeks.

Anthropic, led by CEO Dario Amodei, is reportedly in talks to raise fresh capital at a $350 billion pre-money valuation. That's just four months after hitting $183 billion in September 2025. Nearly a doubling in 16 weeks. That's faster growth than most companies experience in a decade.

Anthropic's Valuation Journey

At current valuations, Anthropic would rank among the ten most valuable companies in the world if it were public. Only Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta, TSMC, and a handful of others exceed that threshold. This is a company that didn't exist three years ago.

But Anthropic Isn't Alone

Elon Musk's xAI recently raised at a $120 billion valuation, making it one of the most valuable private companies in history, though it still trails Anthropic and OpenAI in both valuation and (arguably) model capability.

💡 The Numbers Are Wild

The combined private market value of just three companies (OpenAI ~$157B, Anthropic ~$350B, xAI ~$120B) exceeds $600 billion. That's larger than Sweden's entire GDP.

These are private valuations. When these companies eventually IPO (and they will), the public market frenzy could dwarf anything we've seen since the dot-com era. Whether these valuations hold up post-IPO is another question entirely. I'm skeptical. But that doesn't mean there isn't money to be made on the way up.

2. ASML Gets Its Biggest Upgrade Yet

I've been saying ASML is the most important stock nobody talks about. Now analysts are finally catching up. The Dutch company's extreme ultraviolet (EUV) lithography machines are literally the only way to manufacture cutting-edge semiconductors. There is no substitute. There is no competitor.

This week, Aletheia Capital doubled its price target from $750 to $1,500. That's not a typo. A 2x upgrade is almost unheard of in sell-side research, especially for a company already valued at over $300 billion. ASML stock is up nearly 15% in just three trading days to start 2026.

ASML Key Stats

| Metric | Value |

|---|---|

| 2026 YTD Performance | +14.8% (3 days) |

| EUV Machine Cost | $150+ million each |

| Global Market Share | 100% (EUV) |

| AI Chip Dependency | Nvidia, AMD, all custom silicon requires EUV |

| 2026 Price Target (Aletheia) | $1,500 (2x prior target) |

Every advanced AI accelerator depends on ASML's machines. That includes Nvidia Blackwell, future AMD Instinct chips, and custom silicon from Google, Amazon, and Microsoft. There is no alternative supplier. The stock's blistering start to 2026 proves the market finally believes the AI capex supercycle is structural, not cyclical.

3. Memory Prices & Korean Giants: The Real Money Printer

The AI revolution isn't just enriching chip designers and model developers. It's completely reshaping the memory semiconductor industry. For decades, memory followed a predictable boom-bust cycle: shortage leads to high prices, high prices lead to overinvestment, overinvestment leads to glut, glut leads to collapse. Rinse and repeat every 3-4 years.

But AI might have broken that cycle. HBM demand is relentless. The old rules may no longer apply. Time will tell—but for now, the numbers are hard to argue with.

SK Hynix briefly surpassed every prior peak market cap Samsung Electronics ever achieved in late 2025/early 2026, driven almost entirely by HBM demand for AI training. This one surprised me. SK Hynix, historically the smaller of the two Korean memory giants, is now leading the charge.

Memory Price Explosion

Combined, the two Korean memory leaders now exceed 1,000 trillion won (~$750B+) in market value. Samsung's memory division has become its most valuable asset—more than phones, TVs, or displays combined. Analysts are forecasting Samsung's 2026 earnings to more than double year-over-year, driven primarily by memory.

⚠️ Heads Up for Consumers

Expect phones, laptops, GPUs, and gaming consoles to get noticeably more expensive in the coming months. Memory prices flow through to every electronic device. If you're planning a major tech purchase, sooner is probably better than later.

History rhymes. After shortage comes glut. But most experts see tight supply persisting through at least mid-decade as new fabs take years to come online and AI demand continues to outpace even aggressive capacity expansion plans.

4. Fed Rate Cuts: The Macro Tailwind

And the macro picture? Even better. The Federal Reserve is pivoting dovish, and markets are paying attention.

Current fed funds range: 3.50–3.75%. The latest JOLTS data (November 2025) came in weak, signaling a cooling labor market:

- • Job openings: 7.146 million (vs expected 7.600 million)

- • Significance: Lowest reading since September 2024

- • Trend: Continued softening in labor demand

Here's the Interesting Part

AI-driven productivity gains are deflationary, pushing core inflation metrics toward (or below) the Fed's 2% target. The very technology driving this supercycle is also creating the conditions for lower rates to persist. Powell and the FOMC are watching these productivity improvements closely. They like what they see.

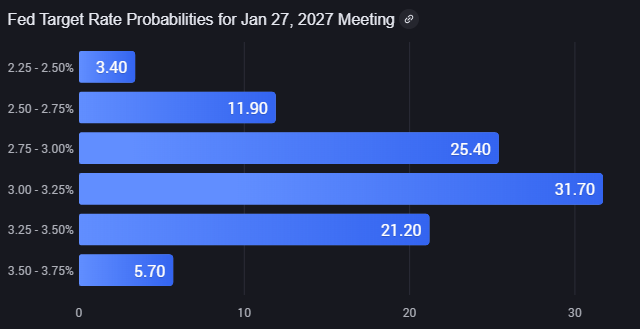

Rate Cut Probability Distribution (Jan 2026 Outlook)

| Target Rate Range | Probability | Cuts from Current |

|---|---|---|

| 3.25% – 3.50% | 23.9% | 1 cut |

| 3.00% – 3.25% | 31.7% ⭐ | 2 cuts |

| 2.75% – 3.00% | 26.1% | 3 cuts |

| 2.50% – 2.75% | 12.8% | 4+ cuts |

Markets are pricing in a high probability of multiple rate cuts by late 2026. The most likely scenario (31.7% probability) sees rates falling to 3.00-3.25%. Combined, there's roughly a 70% chance of at least two cuts by year-end.

Why This Matters for AI Stocks

Lower rates make growth stocks more valuable. That's just math. For AI companies investing billions in infrastructure today but expecting payoffs years from now, the math becomes significantly more favorable when rates drop. This is particularly true for:

- • Hyperscalers (MSFT, GOOG, AMZN) spending $100B+ on AI infrastructure

- • Chip companies (NVDA, AMD, ASML) with multi-year growth runways

- • AI application companies still years away from profitability

Where Does This Leave Us?

Four forces are lining up at once:

The AI supercycle isn't slowing down. If anything, 2026 is shaping up to be the year when these trends accelerate further. We'll see how this plays out. But right now? The setup looks strong.

🎯 My Take

Record private valuations, irreplaceable infrastructure monopolies, surging memory prices, and accommodative Fed policy—it's the most bullish backdrop for AI investing since the sector emerged. Whether the private valuations survive an IPO is anyone's guess. But the capex is real, the infrastructure bottlenecks are real, and the returns for well-positioned investors could be significant.