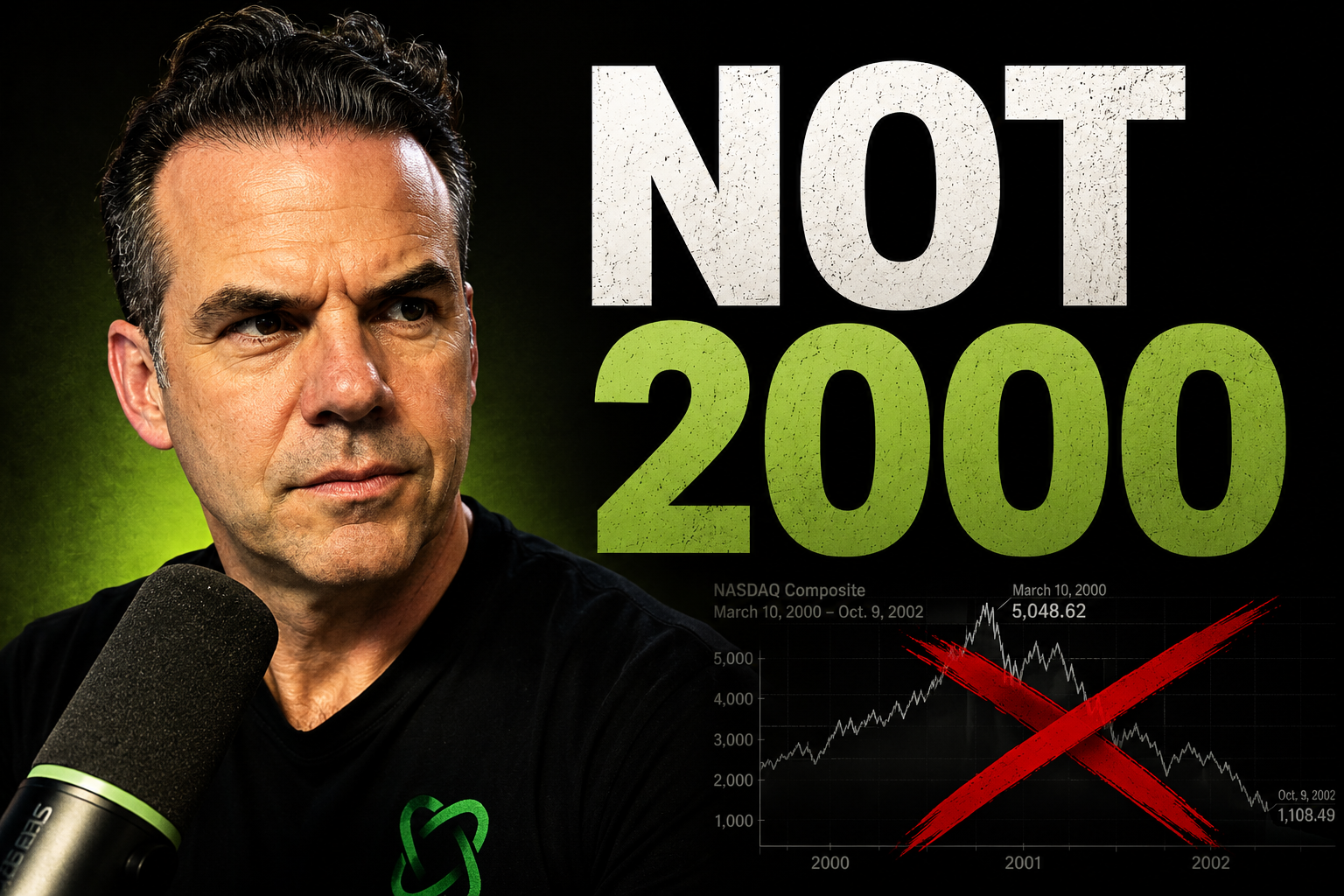

Why This Isn’t the Dot‑Com Bubble

By Cash Flow University · · 7 min read

I break down five concrete differences between the AI boom and the 2000 dot‑com bubble — four favor today, one is a real risk to watch.

Last updated: June 3, 2026

The AI Trade — Five differences that matter

I get the chart-overlay comparison. I overlay the Nasdaq-100 from 1995–2000 on the last three years and it looks familiar: a steep climb, a handful of names, breathless headlines. That visual is a useful prompt for caution. It is not, however, analysis. For traders focused on generating consistent cash flow, understanding the engine under the hood is critical.

Charts show pattern. They do not show cause. When you open the hood, the two cycles are profoundly different. Here are the five differences I care about — and how they inform our trading strategies at Cash Flow University.

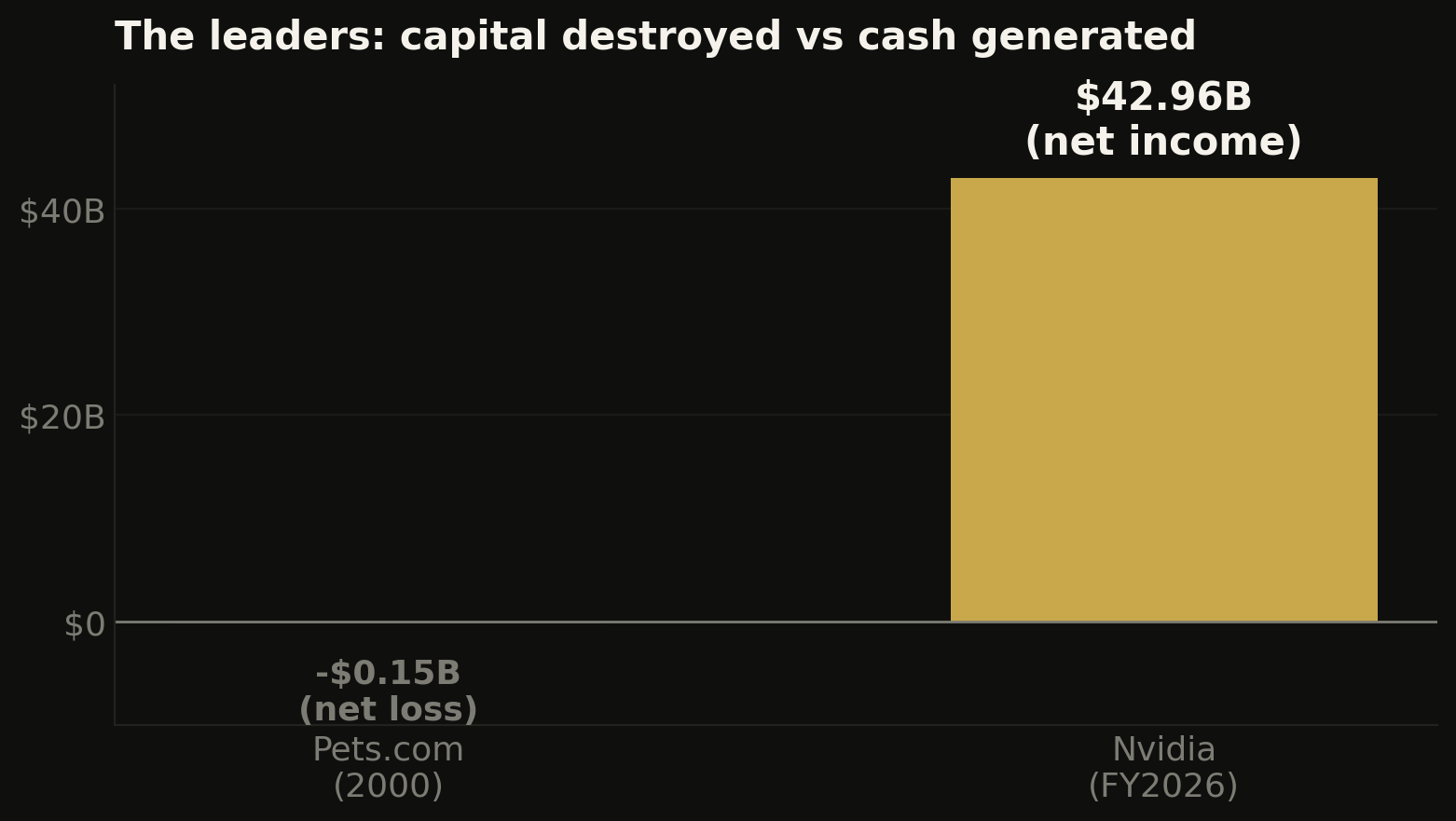

Difference One — The leaders are wildly profitable, not pre‑revenue

The single biggest structural distinction is that today's market leaders are cash-printing machines, not speculative, pre-revenue startups. This is crucial. The dot-com leaders were often burning cash to acquire users, their survival dependent on the next funding round. Today, the names driving the market are built on fortress-like balance sheets.

Nvidia, the obvious example, booked $43 billion of net income in fiscal 2026. A single recent quarter showed profits at a scale most S&P 500 companies never achieve in their entire history.

This doesn't minimize valuation risk. Profitable companies can still be overbought. But a company with trusted, recurring, large-scale profits is not the same animal as a business that disappears when the capital markets get a cold.

Trader's Takeaway: Selling Premium on Quality

For an options trader, this profitability is a green light for income strategies. When a company is fundamentally sound and profitable, it becomes a prime candidate for selling cash-secured puts. If the stock dips, you’re acquiring shares of a great company at a discount. If it stays flat or rises, you keep the premium. It’s a win-win scenario built on a foundation of corporate strength.

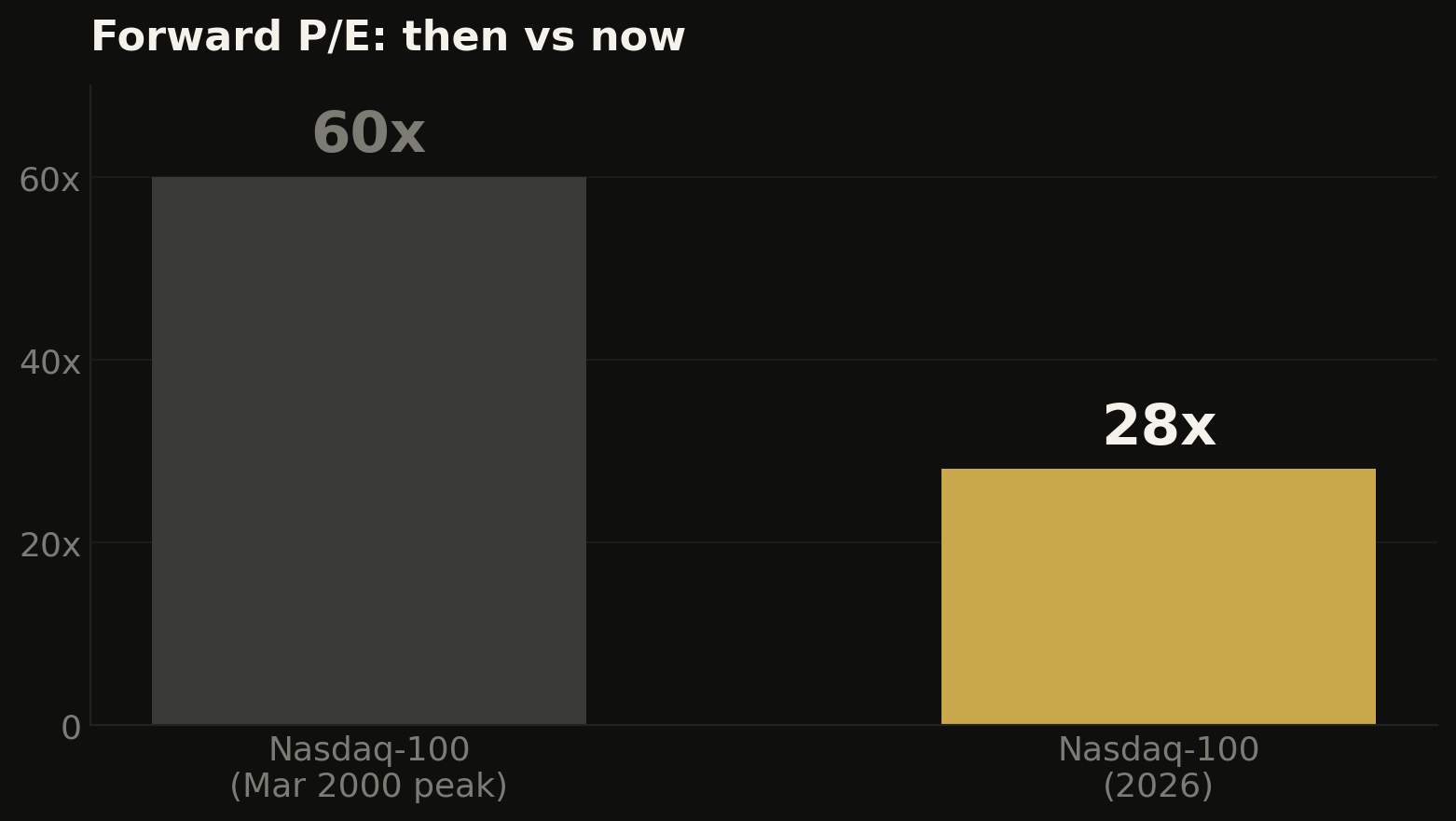

Difference Two — Valuations are high, but far below 2000 peak multiples

Valuations today are elevated, but they are not in the same stratosphere as the dot-com peak. “Expensive” is not equal to “2000‑expensive.” At the height of the bubble, the Nasdaq‑100 traded near an eye-watering ~60x forward earnings. Today, it trades around ~28x forward. To put that in simple terms, you're paying 28 dollars for every one dollar of expected profit next year, not 60. Nvidia itself trades near 40x forward — high, but not a price that requires a decade of flawless execution to be justified.

"A chart overlay tells you two things moved the same way. It tells you nothing about whether the engine underneath is the same. Our job as traders is to underwrite the engine, not chase the chart." - Cash Flow University Methodology

Trader's Takeaway: Generating Income in a Trending Market

In a market with high but not-insane valuations, covered calls are a powerful tool. If you own shares of these strong tech leaders, you can sell call options against them to generate a steady stream of income. This lowers your cost basis over time and pays you while you wait. You cap your upside, but in return, you get immediate, consistent cash flow—the core of our philosophy.

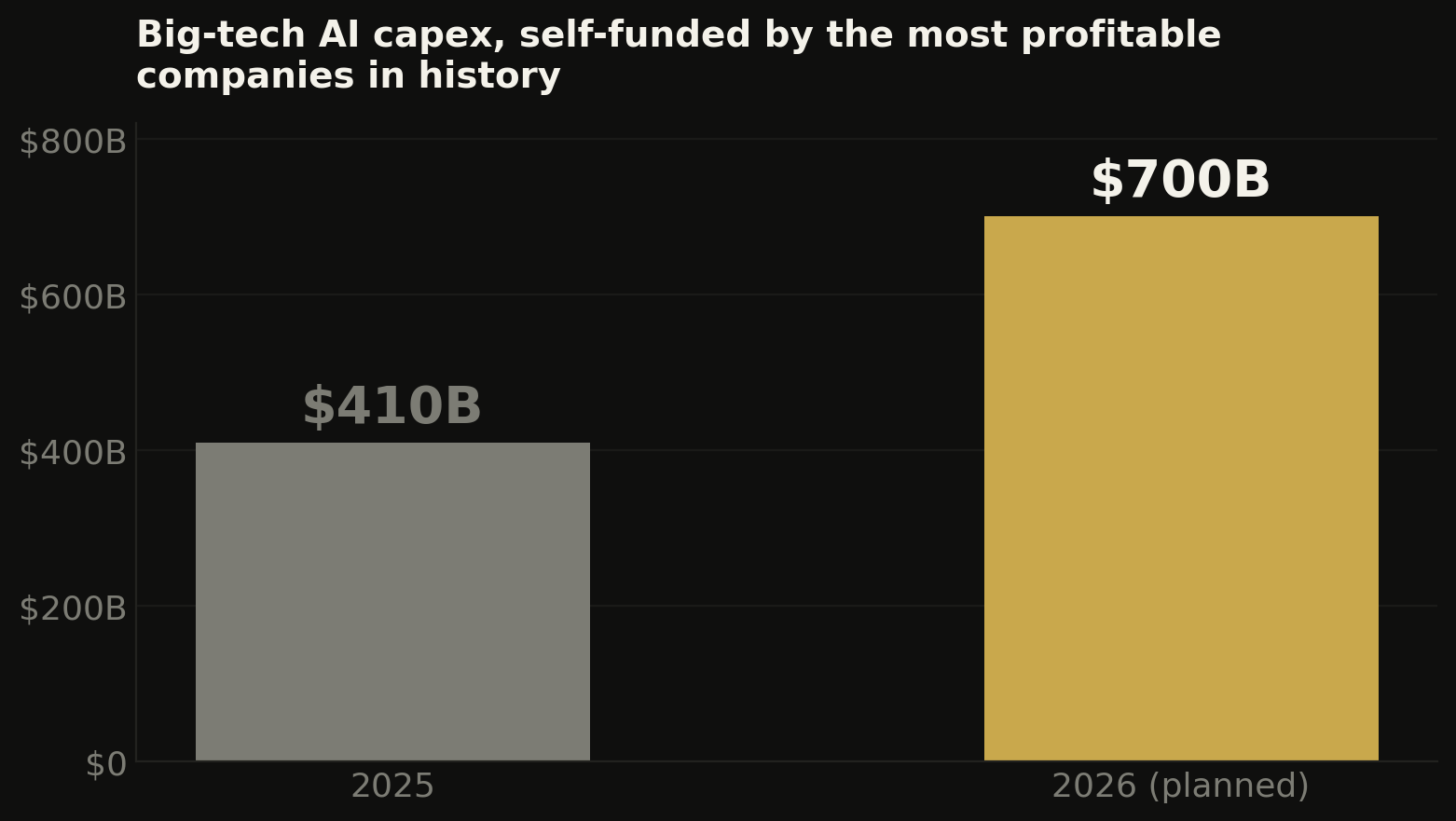

Difference Three — The buildout is largely self‑funded, not by debt or dilution

Today's AI infrastructure buildout is being paid for with operating cash flow, whereas the dot-com boom was fueled by external capital that could (and did) vanish. The web-1.0 era required constant infusions of venture capital and public offerings. When the market turned, the funding dried up, and companies collapsed. Today, the hyperscalers are funding the AI revolution with the money they are already making.

This is a critical difference. A self‑funded investment cycle can be throttled up or down based on demand; it can be preserved during a downturn. A debt-or-equity-funded buildout is a house of cards that collapses when one piece is removed.

Difference Four — Product market traction exists today

Unlike the speculative business models of the dot-com era, the AI industry has provable, large-scale adoption right now. The dot‑com boom was correct about the internet's potential, but many companies were just too early. Their business models depended on a future of high-speed internet and mass adoption that hadn't arrived. AI is different. According to Gartner, global spending on AI a is expected to be over $300 billion in 2026, reflecting real enterprise deployments and production-level spending. That’s the core — adoption is happening at scale.

Trader's Takeaway: Playing the "Picks and Shovels"

This proven adoption means you don't have to bet on the single winning AI application. Instead, you can focus on the "picks and shovels" — the companies providing the essential hardware and infrastructure. This reduces idiosyncratic risk and allows you to trade the broader, more predictable trend of sector-wide investment.

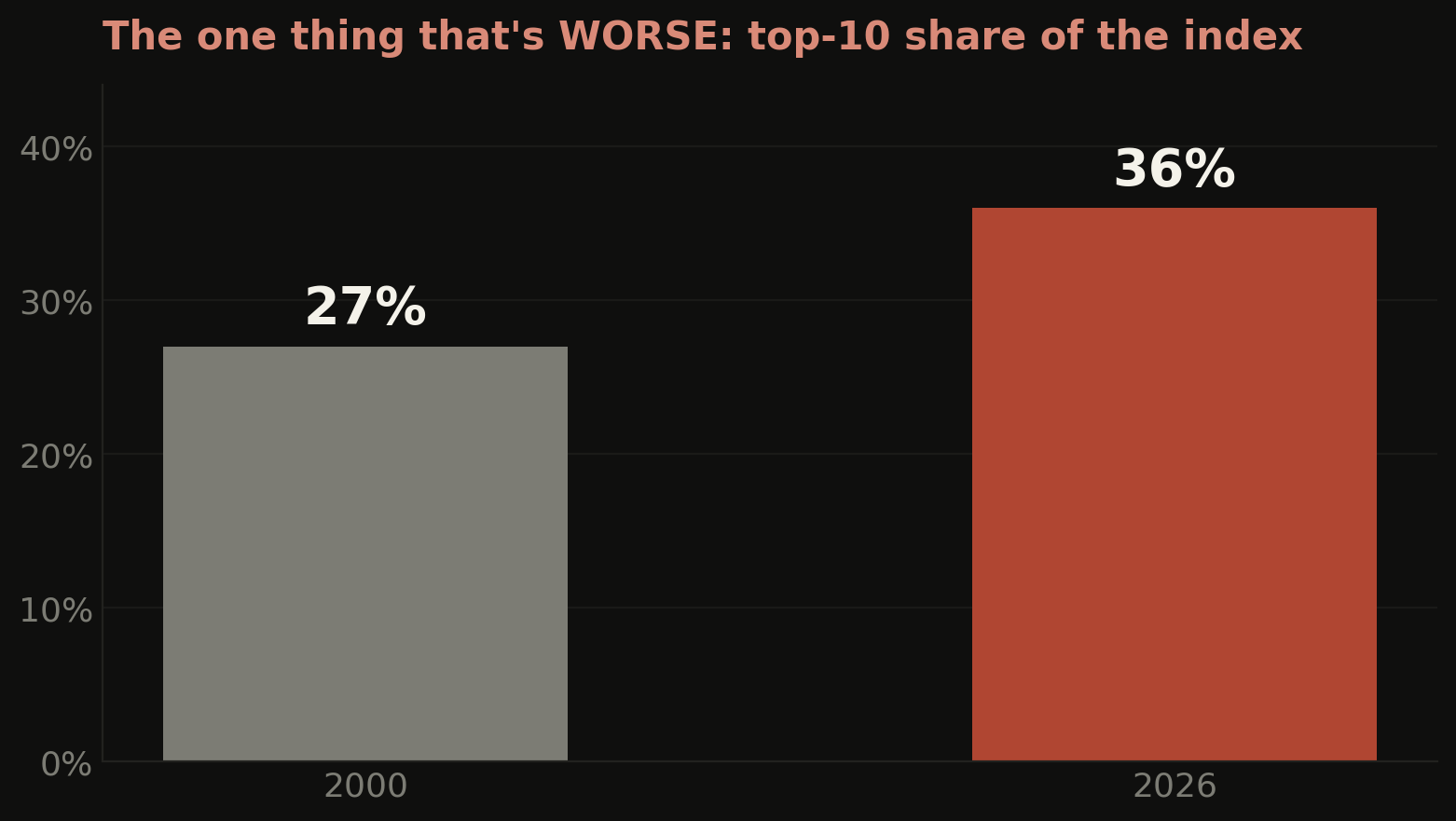

Difference Five — The real risk: concentration

The single biggest risk that is materially worse today is market concentration. If I only listed comforts, I’d be doing the same shallow storytelling the chart-overlayers do. So here’s the real worry that should be top-of-mind for every trader.

There’s another unsettled question: is the incremental AI capacity being built earning enough AI‑specific revenue to justify the spend? The bull case — strong demand scaling into capacity — is plausible and supported by current cash flows. The bear case — too much capacity for the revenue that materializes — is plausible too. That’s why concentration matters: if a handful of names lose their footing, the entire market will feel it keenly.

Trader's Takeaway: Managing Risk with Index Options

When a handful of stocks drive the market, your individual stock portfolio is exposed to systemic risk. This is where index options are invaluable. A study from tastytrade analyzing thousands of trades found that portfolio hedging during periods of high concentration can significantly reduce volatility. Buying puts on an index ETF like QQQ can act as insurance, protecting your tech-heavy portfolio from a broad market downturn caused by a stumble in one or two key names.

Actionable Trading Strategies for Today's Market

Based on this analysis, here are three practical options strategies to consider:

- Sell Cash-Secured Puts on Profitable Leaders: Identify top-tier, profitable companies (like the ones discussed) and sell out-of-the-money puts on pullbacks. This generates income and defines your entry price for a stock you want to own.

- Use Covered Calls for Income Generation: If you already own 100+ shares of these leading tech stocks, sell call options against your position to create a recurring income stream, effectively getting paid while you hold.

- Hedge Your Portfolio with Index Puts: Given the concentration risk, regularly assess your portfolio's exposure. Consider buying puts on the Nasdaq-100 (via QQQ) as a cost-effective way to insure against a sector-wide correction.

FAQ – Navigating the AI-Driven Market

- Is it too late to invest in AI stocks?

- It's not about being "late," but about being "smart." Chasing parabolic moves is a losing game. A better approach is to use options to get paid to wait for your price on high-quality names or to generate income from stocks you already own. Focus on strategy, not timing.

- What's the biggest mistake a trader can make in this environment?

- The biggest mistake is ignoring risk management. High concentration and elevated valuations mean you must know your exposure and have a hedging strategy. Assuming the trend will continue forever without preparing for a pullback is a recipe for disaster.

- How can options help if I don't want to buy expensive tech stocks outright?

- Options are perfect for this. You can use defined-risk spreads, like bull call spreads or bear put spreads, to make directional bets with a limited, pre-defined risk. This allows you to participate in the moves of expensive stocks without the massive capital outlay of buying shares directly.

Bottom line: the right frame is not “bubble” vs “no‑bubble.” It’s a tradeoff of probability, price, and exposure. We see structural advantages relative to 2000: real profits, lower peak multiples, self‑funded capex, and mass adoption. We also see clear risks in concentration. This doesn't mean run for the hills; it means trade smarter. By using options strategies to manage risk, generate income, and define your entries, you can navigate this powerful trend without falling victim to its potential excesses.

At Cash Flow University, we run our portfolio the same way we teach: know what you own, understand the risks, and use the right tools to get paid for the risk you take.